![]()

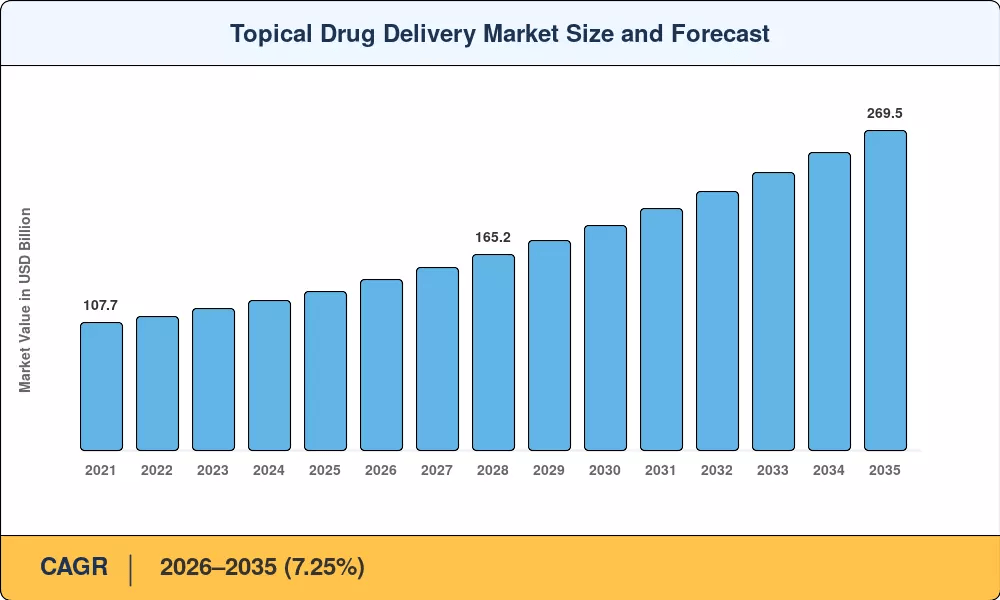

Topical Drug Delivery Market to Surge from USD 143.60 Billion in 2026 to USD 269.50 Billion by 2035—Powered by FDA Non-Opioid Analgesic Pathway Incentives

NY, CA, UNITED STATES, June 18, 2026 /EINPresswire.com/ — As per Market Research Future, the global Topical Drug Delivery Market size to reach USD 269.50 Billion by 2035 from USD 143.60 Billion in 2026, at a CAGR of 7.25% during the forecast period 2026–2035. The market base was estimated at USD 133.90 Billion in 2025.

The 7.25% CAGR—anchored by structural dermatological and pain-management demand rather than discretionary healthcare spending—is driven by three converging forces: the FDA’s expanded guidance on non-opioid analgesic approvals that has accelerated clearance timelines for transdermal drug absorption platforms, sustained microneedle and nano-carrier platform advances that have pulled dermal permeation enhancement technologies into routine procurement cycles, and connected health smart patch ecosystems that have converted localized skin drug therapy from passive dispensing into real-time adherence monitoring and data monetization platforms.

National governments and multilateral health organizations are amplifying this momentum. The WHO estimates that skin diseases affect people globally at any given time, a figure that has climbed 15% over the past decade due to aging demographics and environmental stressors. The U.S. FDA’s 2024 guidance on expedited review for non-opioid transdermal analgesics reduced mean approval timelines by an estimated 8–10 months for qualifying applications.

The European Commission earmarked EUR 1.2 Billion through Horizon Europe for advanced skin patch medication delivery technologies through 2027. The global dermal permeation enhancement technology pipeline saw USD 4.8 Billion in cumulative private investment between 2022 and 2024. Together, these initiatives are creating the procurement infrastructure and delivery innovation on which the Topical Drug Delivery Market depends.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/33250

Key Market Trends & Growth Drivers

FDA Non-Opioid Analgesic Pathway Incentives and Regulatory Support

Regulatory pathways increasingly favor streamlined review frameworks for non-opioid transdermal drug absorption platforms, with the FDA’s 2024 guidance on expedited review for non-opioid transdermal analgesics reducing mean approval timelines by an estimated 8–10 months for qualifying applications. Similarly, the EMA’s revised 2023 Guideline on Quality of Transdermal Patches tightened bioequivalence standards while introducing accelerated pathways for dermal permeation enhancement technologies that demonstrate superior pharmacokinetic profiles. These dual-continent incentives are pulling investment toward localized skin drug therapy platforms designed for pain management.

CMS reimbursement expansion for remote therapeutic monitoring (RTM) codes—covering topical and transdermal devices—signals payer willingness to fund connected care models that track localized skin drug therapy compliance in real time. Payers in high-income countries now authorize an average of 3.2 topical prescriptions per diagnosed dermatology patient annually, generating a durable volume floor for the topical drug delivery market. Early-adopter health systems report that the convergence of flexible electronics, printed biosensors, and adhesive science is creating a platform model where a single smart-patch architecture supports multiple drug cartridges.

Microneedle & Nano-Carrier Platform Advances

Legacy ointments and generic creams are yielding ground to precision-engineered delivery architectures. Microneedle arrays, nano-emulsion carriers, and sensor-enabled wearable patches are displacing first-generation topical cream formulation approaches that rely on passive diffusion alone. Global venture and corporate investment in microneedle platforms exceeded USD 1.6 Billion cumulatively through 2024, with dissolving-tip arrays and hydrogel-forming designs leading translational pipelines. Nano-carrier systems—liposomes, solid lipid nanoparticles, and polymeric micelles—further improve transdermal drug absorption by enabling controlled release of macromolecules through the stratum corneum.

Pooled procurement through hospital group purchasing organizations drives per-unit prices down for high-volume topical cream formulations, expanding access while compressing manufacturer margins. These advances collectively shrink the efficacy gap between topical and systemic delivery, unlocking indications that were previously injection-only. Early-phase clinical data for topical anti-IL-17 gels show similar efficacy to subcutaneous injection for mild-to-moderate psoriasis, a game-changing value proposition for the topical drug delivery market. In the US, microneedle adoption is accelerating as dermatology clinics seek needle-free alternatives to biologic injections.

Connected Health Smart Patch Ecosystems and Home-Care Expansion

Sensor-enabled skin patch medication delivery devices that wirelessly transmit adherence and pharmacokinetic data to clinician dashboards accounted for an estimated USD 2.1 Billion in combined R&D spending globally in 2024. The U.S. CMS reimbursement pilot for remote therapeutic monitoring (RTM) codes—covering topical and transdermal devices—signals payer willingness to fund connected care models that track localized skin drug therapy compliance in real time. Smart patches generating real-time compliance data allow a subscription-based business model—hardware plus data analytics—increasing per-patient lifetime value by approximately 25–35% over single-dispense economics.

The shift toward home-care and self-administration models is transforming the topical drug delivery market. Localized skin drug therapy regimens—once initiated in the clinic—transfer seamlessly to patient self-management. Smart skin patch medication delivery devices with app-based reminders further support adherence in the home setting. Home-care settings are growing at a 9.68% CAGR, the fastest among end-user channels, as patients increasingly manage localized skin drug therapy outside hospital walls. By 2030, the skin patch medication delivery ecosystem is expected to generate recurring data-analytics revenue that could equal 15–20% of device hardware sales.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/33250

Market Segment Insights

BY ROUTE OF ADMINISTRATION

Dermal: Dominant segment with ~48.2% revenue share in 2025. Reflecting the dominance of creams, gels, and ointments in chronic dermatological care. The dermal route continues to anchor the topical drug delivery market because it addresses the broadest therapeutic surface area—psoriasis, atopic dermatitis, acne, and wound care—using well-understood topical cream formulation platforms.

Nasal: Fastest-growing route segment at 9.85% CAGR (2026–2035). Fueled by migraine and CNS drug pipelines that leverage transdermal drug absorption pathways. Nasal delivery is the fastest-growing route, driven by needle-free vaccine programs and migraine treatments that exploit mucosal transdermal drug absorption for rapid systemic onset.

Ophthalmic: USD 24.85 Billion in 2025. Glaucoma and dry-eye pipelines sustain demand for topical ocular drug delivery.

Others (Rectal, Vaginal, Otic): USD 14.73 Billion in 2025. Localized infection therapeutics represent incremental demand channels.

BY PRODUCT

Formulations (Solid, Semi-Solid, etc.): Dominant segment with ~75.6% revenue share in 2025. Reflecting established manufacturing infrastructure and low-cost production. Traditional formulations—ointments, creams, gels, and lotions—dominate the topical drug delivery market by volume, benefiting from low-cost production and wide prescriber familiarity.

Devices (Transdermal Patches, etc.): Fastest-growing product segment at 8.72% CAGR (2026–2035). Smart-patch and microneedle innovation drives demand. The devices segment, encompassing advanced skin patch medication delivery platforms and microneedle arrays, is gaining share as dermal permeation enhancement technology enables controlled, sustained-release dosing that traditional semi-solids cannot match.

BY INDICATION

Dermatology: Dominant indication with ~45.4% revenue share in 2025. Reinforcing its role as the primary therapeutic arena for topical cream formulation innovation. Psoriasis, eczema, and acne prevalence create a massive addressable patient pool for localized skin drug therapy.

Pain Management: Fastest-growing indication segment at 10.70% CAGR (2026–2035). Non-opioid patch regulatory incentives drive demand. Pain management is the fastest-growing indication, reflecting strong regulatory tailwinds for non-opioid transdermal drug absorption alternatives. Localized skin drug therapy for musculoskeletal pain—diclofenac patches, lidocaine systems—captures both prescription and OTC channels.

Others (Hormonal, Cardiovascular, etc.): USD 32.60 Billion in 2025. Hormone-replacement and anti-anginal patches sustain residual demand.

BY END USER

Hospitals: Largest segment at ~37.8% share in 2025. In-patient wound care and post-surgical protocols dominate volume, channeling routine localized skin drug therapy supply.

Home-Care Settings: Fastest-growing end-user segment at 9.68% CAGR (2026–2035). Patient self-administration and telehealth drive demand. Home care is the fastest-growing end-user channel because localized skin drug therapy regimens transfer seamlessly to patient self-management.

Specialty Clinics & Others: USD 36.20 Billion in 2025. Dermatology and pain-management clinics represent incremental demand channels.

BY DISTRIBUTION CHANNEL

Retail Pharmacies: Dominant channel with ~42.5% share in 2025. OTC topical cream formulation dominance and prescription fulfillment anchor this segment.

E-commerce: Fastest-growing channel at 11.2% CAGR (2026–2035). Direct-to-consumer skin patch medication delivery and telehealth integration drive demand.

Hospital Pharmacies: USD 28.40 Billion in 2025. Inpatient and outpatient prescription dispensing sustains demand.

Clinics: Growing segment at 7.8% CAGR (2026–2035). Dermatology and pain-management clinic dispensing drives demand.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/topical-drug-delivery-market-33250

Regional Outlook

North America — Dominant Market (~41.3% Share, 2025)

The United States generates approximately 82.4% of North American Topical Drug Delivery Market revenue, driven by FDA non-opioid transdermal drug absorption incentives, CMS reimbursement expansions for remote therapeutic monitoring, and a 340B program that channels discounted topical biologics to safety-net hospitals—a single policy ecosystem that converted a generic-cream-dominated market into one with a structural smart-patch and connected-health tail.

The US dominates through a combination of robust payer coverage for localized skin drug therapy, a dense clinical-trial infrastructure, and rapid adoption of novel dermal permeation enhancement technologies.

Europe — Second Largest (~27.5% Share, 2025)

Europe’s Topical Drug Delivery Market reflects divergent national strategies—Germany leads regionally with statutory-insurance coverage of dermal permeation enhancement patches at 7.42% CAGR, while the UK historically used selective topical targeting before broadening coverage through the NHS Long-Term Plan skin-disease funding at USD 5.88 Billion in 2025.

France contributes ~15.8% of regional share through a national biosimilar substitution mandate. Italy contributes ~11.2% of regional share on hospital-based dermatology centers of excellence. Spain contributes USD 3.10 Billion on OTC topical growth in the pharmacy channel.

Asia-Pacific — Fastest-Growing Region (9.90% CAGR, 2026–2035)

Asia-Pacific is the engine of the Topical Drug Delivery Market. China holds the largest regional share with ~32.4% of regional revenue, driven by NRDL topical drug additions and expanding insurance pools.

India is growing at 10.15% CAGR on the back of Ayushman Bharat coverage expansion for over 500 million citizens, creating volume runways for localized skin drug therapy items in price-sensitive countries. Japan contributes USD 5.52 Billion through aging population and high patch adoption at steady pace. South Korea holds ~7.8% of regional share on K-beauty crossover into medicated topicals.

Middle East & Africa — Emerging Opportunity (8.45% CAGR, 2026–2035)

The Middle East & Africa carries the widest access gap and therefore the steepest opportunity. Saudi Arabia leads the region with Vision 2030 pharma localization, contributing ~28.5% of regional share—the National Industrial Development and Logistics Program targets 40% local pharmaceutical manufacturing by 2030, creating incentives for topical cream formulation plants that serve both domestic and regional export demand.

The UAE is growing at 8.45% CAGR on medical-tourism dermatology clinics. South Africa holds ~18.6% of regional share on public-sector dermatological formulary expansion.

South America — Growing Presence (USD 6.96 Billion, 2025)

Brazil anchors South America’s Topical Drug Delivery Market at ~58.3% of regional revenue, with the SUS public-health system adding four topical corticosteroid formulations to its essential medicines list in 2024, broadening access to localized skin drug therapy for approximately 160 million public-system beneficiaries and providing a stable demand floor that smooths regional forecasts. Argentina is growing at 7.62% CAGR on localized skin drug therapy awareness campaigns.

Competitive Landscape and Recent Developments

The Topical Drug Delivery Market exhibits medium concentration, with the top five companies holding an estimated 28–34% combined revenue share. The Herfindahl-Hirschman Index (HHI) sits in the 600–900 range, indicating a moderately fragmented landscape where large pharmaceutical incumbents compete alongside specialty device firms and regional generics houses. Patent portfolios around novel excipient blends and device-design patents on patch architectures create layered IP moats that extend exclusivity windows beyond single-patent lifetimes.

The competitive landscape is stratified between broad OTC and Rx topical portfolio leaders serving global dermatology markets, patch technology specialists capturing transdermal tenders, and pure-play dermatology focus providers consolidating the aesthetic and medicated topical segment.

KEY COMPANIES AND RECENT MILESTONES

Johnson & Johnson (2024–2025): Maintains leadership with Neutrogena dermatologicals and Lidocaine patches, commanding ~7–10% of global Topical Drug Delivery Market revenue. Broad OTC and Rx topical portfolio serves global consumer and prescription markets.

Novartis AG (2024–2025): Dermatology biologics and ophthalmic drops anchor a strong biologics pipeline leader positioning, holding ~5–8% of global revenue. The company benefits from the structural biologic topical tail created by expanding precision dermatology pipelines.

GSK plc (2024–2025): Corticosteroid creams and antiviral topicals anchor a strong global OTC distribution strength positioning, holding ~4–7% of global revenue.

Bayer AG (2024–2025): Dermatology OTC and wound-care topicals anchor a strong consumer-health brand leverage positioning, holding ~3–6% of global revenue.

Future Outlook: 2026–2035

By 2030, AI-optimized formulation design and wearable-patch platform economics will become the operating system of topical drug delivery. Machine-learning models trained on skin-permeation datasets are compressing topical cream formulation development from 18-month bench cycles to under 90 days in early adopter labs.

AI-guided excipient screening improves first-pass clinical success rates for transdermal drug absorption platforms by an estimated 20–30%, cutting per-compound development costs substantially. The convergence of flexible electronics, printed biosensors, and adhesive science is creating a platform model where a single smart-patch architecture supports multiple drug cartridges. By 2030, the skin patch medication delivery ecosystem is expected to generate recurring data-analytics revenue that could equal 15–20% of device hardware sales.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/transdermal-drug-delivery-systems-market-7545

https://www.marketresearchfuture.com/reports/drug-delivery-devices-market-11841

https://www.marketresearchfuture.com/reports/controlled-release-drug-delivery-market-6794

https://www.marketresearchfuture.com/reports/nanotechnology-based-drug-delivery-market-34011

https://www.marketresearchfuture.com/reports/injectable-drug-delivery-devices-market-1211

https://www.marketresearchfuture.com/reports/microneedle-drug-delivery-system-market-33688

https://www.marketresearchfuture.com/reports/dermal-fillers-market-3893

https://www.marketresearchfuture.com/reports/topical-corticosteroids-market-4331

https://www.marketresearchfuture.com/reports/advanced-drug-delivery-market-35801

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery